4 ways the hierarchy of construction OEMs could change amid tech challenges

14 July 2023

Since its launch in the 1990s, the KHL Yellow Table has become the standard reference in the industry, tracking the size of the world’s 50 biggest OEMs by revenue. But at a time of unprecedented technical and business model change, who are likely to be the winners and losers in Yellow Tables to come? Alan Berger and Carl Gustaf Göransson from commercial vehicle advisory firm abcg have dusted off their crystal ball to suggest what future Yellow Tables might look like.

Image: AdobeStock

Image: AdobeStock

Prediction is very difficult, especially when it’s about the future, as the old joke goes. But in this case it’s probably best to start by doing the opposite and looking to the past.

Over the years, we have seen OEMs move from relative obscurity to the top 10 of the Yellow Table, while some early top 10 players have dropped (Do you remember when Ingersoll Rand and Terex were in the top 10?).

All players have grown with the market, and for sure some have taken relative market share.

But all in all, most of the movement in recent years has come from either relative movement of individual markets or M&A activity.

Since most OEMs are stronger in one or two regions than the others (Caterpillar in the US, Komatsu in Japan, Sany in China etc.), a strong year (or decade) for a region can propel an OEM up the rankings.

Obviously, the opposite also holds true. Chinese OEMs, for example, moved up 2021’s table as domestic demand remained strong in a relatively weak global market, but only to slide back down again when the tables turned in the latest list.

Carl Gustaf Göransson (Image supplied)

Carl Gustaf Göransson (Image supplied)

Spending money helps buy yourself promotion too - Deere’s acquisition of Wirtgen propelled it six places higher overnight.

Similarly, Volvo CE also became a player when it spent the proceeds of selling its car division and hoovered up multiple brands (including Samsung’s excavator business) over 20 years ago.

While Europe, North America and China will continue to have their ups and downs relative to each other, we believe those will be relatively small in total impact going forward.

But this story ignores the world’s most populous country – India.

Just like China has dominated the global growth story for the past 10 years, it appears that India is poised to accelerate.

Local presence has an impact and both JCB’s and Hitachi’s market position reflects their long history in the country.

Unlike China, domestic Indian OEMs are relatively small and some of the global players are entrenched.

India’s ascendance is likely to propel JCB solidly into the top 10, while potentially also moving Hitachi upward as well. Overall, OEMs can maintain a strong global position by focusing on one or two major regions that are aligned with their natural strengths.

The ‘triple technology challenge’

If the industry were in a relatively stable state, this analysis might be sufficient.

Alan Berger (Image supplied)

Alan Berger (Image supplied)

But we contend that the ‘triple technology challenge’ – automation and connectivity, alternative fuels and corresponding business model shifts – that the industry is in the midst of, is a new factor that could re-order the competitive hierarchy.

These changes will impact the product design and how OEMs take their products to market, providing room for changes in the competitive hierarchy.

We have argued elsewhere that the Chinese OEMs have a natural advantage on electrification, given the intense focus on the electric automotive ecosystem that exists in China, while some of the European OEMs have made a deep commitment to electrified machines (for example, Volvo CE with its compact equipment.)

That said, the huge investments required to succeed are likely to drive some level of partnership or consolidation. Particularly among the mid-size and smaller OEMs that are struggling to keep their product line current and integrate the new technologies.

Bringing this all together, we see several potential scenarios, going from the relatively boring ‘status quo’ – where most OEMs manage the triple technology challenge all equally well – to an industry shake-up where the Chinese OEMs dominate the top 10.

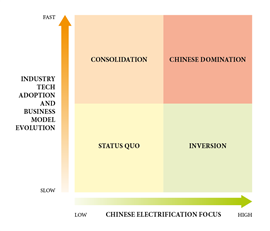

The figure below maps out the potential scenarios along two major axes. The extent that Chinese companies capitalize on the electrification strengths their automotive counterparts have created along the horizontal direction and the speed in which the new technologies and corresponding business model changes are adopted by the end customers.

Scenarios

Source: abcg

Source: abcg

This results in four scenarios as the extremes:

1) Consolidation: Creates more focused specialization, such as a few major compact equipment players and a few dominant large equipment companies. This naturally follows the faster than overall market growth of compact equipment. The main consolidation comes from the mid-sized and smaller players that need to combine to gain synergies and scale in investments.

2) Chinese domination: China has strategically targeted passenger car electrification, creating the most robust ecosystem for electric vehicles. In this scenario, the market moves quickly and Chinese OEMs leverage their local electro-ecosystem to displace slower moving global players, resulting in Chinese OEMs taking over a significant portion of the top 10.

3) Inversion: While technology adoption moves slowly, the high focus on electrification in China enables the smaller Chinese OEMs to move up significantly in the Yellow Table.

4) Status Quo: Here the triple technology challenge evolves so slowly in the market that the usual drivers – relative market size and M&A activity will set the direction.

The triple technology challenge brings a new dynamic to the traditional market size and M&A drivers of industry movement. Those OEMs that are currently in comfortable positions in the Yellow Table might find themselves moving significantly downward if they don’t manage this evolving scenario well and quickly.

With no clear scenario looking more likely than the others, predicting about the future has never been trickier.

So, who will win? As the old cliché goes – only time will tell.

Alan Berger and Carl Gustaf Göransson are managing partners of the commercial vehicle advisory practice abcg.

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

POWER SOURCING GUIDE

The trusted reference and buyer’s guide for 83 years

The original “desktop search engine,” guiding nearly 10,000 users in more than 90 countries it is the primary reference for specifications and details on all the components that go into engine systems.

Visit Now

CONNECT WITH THE TEAM